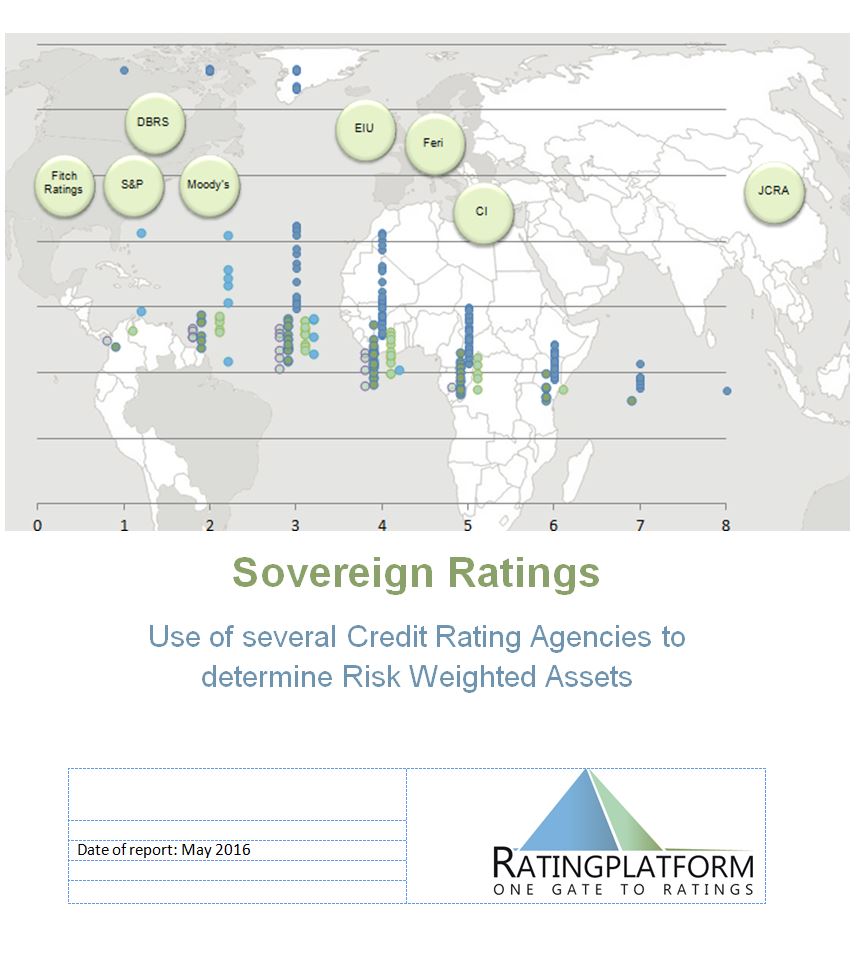

In this research report, we take the perspective of an investor having a portfolio of sovereign assets based on each countries share in the IMF capital (measured at the Special Drawing Rights level – SDR). Using the IMF SDRs provides a constant basis of comparison and excludes exchange rate changes as well as changes in the composition of the assets – this allows focusing the attention on the rating activity of Credit Rating Agencies (CRAs) and how this impacts on Risk Weighted Assets (RWAs)

Our analysis is based on 8 ESMA registered CRAs and covers year end ratings for the period 2013 to 2015. Given that the vast majority of ratings fall into the lowest Risk Weight (RW) of 0%, our global investor will see RWA decreasing whatever CRA is being used. The RWAs decrease as the rated universe of the respective CRA increases: the higher the coverage, the lower the RWAs. In case our investors uses more than 2 CRAs, given that the ECAI rules require the use of the second best rating (measured at the level of the Risk Weight) and the continuous use of the nominated ECAIs, we find that using all CRAs reduces and stabilizes RWAs over time. The report costs EUR 750,- (excl. VAT). The applicable VAT rate in Austria is 20%. For Clients domiciled in the EU, if you can provide your valid VAT- ID, we shall issue the invoice without VAT. For Clients based outside of the EU, no VAT is charged.